As we near and enter retirement, there are two investment strategies that one can choose from: total return investing or income investing. While investment advisors can differ on which approach is better, the majority favor total return investing for retired and near-retired investors. This month we’ll take a look at the reasons for this. Let’s begin by briefly explaining these two approaches.

Total Return Investing

Total return investing is an investment strategy that focuses on the overall return of a portfolio — the combination of capital appreciation (the increase in the value of investments) and income (dividends, interest and other distributions).

Income Investing

Income investing is an investment strategy focused on generating a steady stream of cash payments from your investments rather than primarily seeking growth in their value. The goal is to create regular income from sources such as: dividends from stocks, interest from bonds and CDs, distributions from REITs (Real Estate Investment Trusts) and income from certain mutual funds and ETFs (Exchange-Traded Funds).

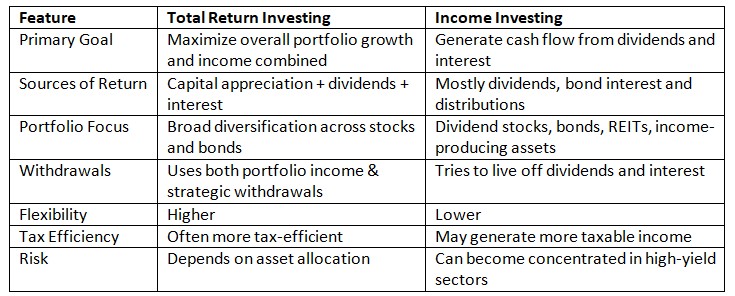

Comparing Both Approaches

Here’s a quick comparison of these two approaches to retirement investing.

Why Choose Total Return Investing

People who favor income investing, often believe in the old adage that it’s best to leave principal untouched. People who favor total return investing focus on how their portfolio can sustainably support their spending needs throughout retirement (instead of how much income does their portfolio generate). And really, shouldn’t running out of money in retirement be the focus?

Choosing one of these approaches is obviously step one. After that there are many, many details involved in constructing a portfolio that will protect you and your family through your entire retirement. If you’d like some help thinking about all of this, or any other financial matters, we’d be happy to get together in a no-charge, no-obligation initial meeting. Please visit our website or give us a call at 970.419.8212 to set up an in-person or virtual meeting.

This article is for informational purposes only. This website does not provide tax or investment advice, nor is it an offer or solicitation of any kind to buy or sell any investment products. Please consult your tax or investment advisor for specific advice.